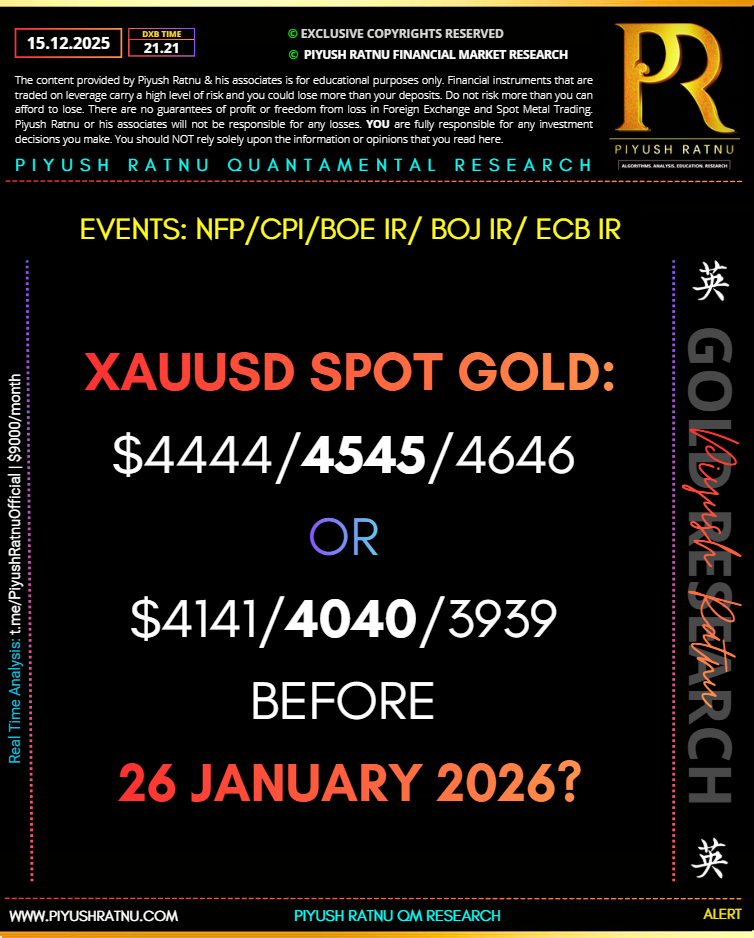

How to trade XAUUSD Spot Gold accurately after NonFarm Payrolls NFP Data December 2025?

XAUUSD Spot Gold: $4444/4545/4646 or $4141/4040/3939 before 26 January 2026?

Economic data takes centre stage this week, with markets facing a backlog of delayed US releases alongside the final round of central bank decisions for the year. In the UK, rates markets are almost fully committed to a move, pricing an 87% probability of a Bank of England cut next week after the economy contracted for a second straight month in October. With CPI and labour market data due before the Christmas break, sterling remains highly exposed to downside surprises.

Economic data takes centre stage this week, with markets facing a backlog of delayed US releases alongside the final round of central bank decisions for the year. In the UK, rates markets are almost fully committed to a move, pricing an 87% probability of a Bank of England cut next week after the economy contracted for a second straight month in October. With CPI and labour market data due before the Christmas break, sterling remains highly exposed to downside surprises.

The US calendar is equally heavy. November payrolls hit on Tuesday, alongside October retail sales and November CPI. With rate-cut expectations for 2026 still stretched, the dollar is set up for volatility: firm data would push US yields higher and force a repricing in favour of USD, while weaker numbers would keep the pressure on.

Central banks add another layer of risk. The ECB is expected to stand pat and signal a prolonged pause in its easing cycle—an outcome that does little to help the euro, particularly if growth momentum continues to lag. Meanwhile, the Bank of Japan is expected to deliver a 25bp hike to 0.75%, reinforcing the slow and uneven normalisation of policy and keeping the yen sensitive to any upside surprise in rates or guidance.

Only strong data will drag the market back into line with the Fed’s view – Piyush Ratnu Gold Market Research

Bond markets were calm last week, but that complacency is likely to be tested. A heavy slate of central bank decisions and top-tier economic data this week could force a reset in 2026 rate-cut pricing across the majors. Fed funds futures are still leaning dovish, pricing two Fed cuts next year—one more than the FOMC is signalling. That gap leaves the dollar exposed. US Treasuries can stay bid only if labour market data weakens convincingly. Any evidence of renewed strength in jobs would quickly strip out excess easing bets, lift US yields, and underpin the dollar.

The US Treasury market has been one of the strongest performers globally in 2025, with gilts and Canadian bonds close behind. A renewed push higher in Treasury yields would almost certainly drag UK and Canadian yields with it, limiting downside in GBP and CAD. By contrast, European bonds have lagged, and that underperformance looks set to continue. If the ECB flags a prolonged pause in its easing cycle, euro area yields could grind higher, but without the same growth support—an unfavourable mix for the euro and one that keeps EUR rallies on a short leash.

Right now, the market is still leaning more dovish than the Fed, with futures pricing more cuts than the FOMC is signalling. That disconnect can persist while growth data is mixed. But it becomes unstable if the US labour market and inflation prints refuse to soften.

If payrolls hold up, unemployment stays low, and core CPI remains sticky, the market will have little choice but to fall in line with the Fed. That means fewer cuts priced for 2026, higher front-end yields, a flatter curve, and a firmer dollar. In that scenario, the Fed doesn’t need to talk tougher—the data does the work.

If, however, jobs data weakens decisively and inflation continues to trend lower, the market won’t follow the Fed; it will drag the Fed towards it. Rate-cut expectations would stay elevated, yields would struggle to rise, and the dollar would remain on the back foot.

Bottom line: this is a data-led standoff. The Fed is holding the line, but the market only capitulates if the US economy refuses to slow. This week’s labour and inflation data are the trigger.

FX WEEKLY: DATA FORCES THE REPRICING

This week is about whether markets finally capitulate to central bank reality. Volatility is underpriced. Positioning is stretched. Correlations matter again.

1. US DATA DUMP — USD DIRECTIONAL RISK IS ASYMMETRIC

The backlog of US data hits all at once, led by November payrolls and CPI. This is the first meaningful labour market read since before the government shutdown and includes residual October effects—translation: noise risk is high, but direction matters more than precision.

Consensus payrolls sit at ~50k, unemployment at 4.5%, and earnings at 3.6% y/y. That wage number is still incompatible with a rapid easing cycle. Any upside surprise—jobs, wages, or participation—forces a front-end rates repricing, pushing 2-year yields higher, flattening the curve, and dragging USD higher across the board. In FX terms:

-

USD strength expresses fastest vs EUR and JPY

-

High-beta FX underperforms as real yields rise

CPI is expected to confirm that disinflation has stalled. Both headline and core are forecast to stay above 3%, keeping the Fed boxed in. The correlation is clean: sticky CPI → higher real rates → stronger USD. The downside for the dollar only opens if both payrolls and CPI miss meaningfully—and that bar is high.

Bias: USD upside skew remains intact.

2. BOE CUT — GBP LIVES AND DIES BY FORWARD GUIDANCE

The Bank of England is expected to cut rates to 3.75%, with Bloomberg showing unanimous economist expectations. We see a narrow 5–4 vote. This is not a growth rescue—it’s damage control.

The UK macro setup is fragile: contracting output, rising unemployment (expected 5.1%, highest since 2021), and inflation that is easing but still uncomfortably high. Rate cuts won’t fix that. Fiscal already fired its shot. The BOE is next—and markets are demanding delivery.

For FX, the cut itself is priced. GBP trades the path, not the move. If the BOE pushes back against expectations for the next cut (currently June), front-end gilt yields hold up, and GBP stabilises via rate-differential support. If the BOE validates the easing path, GBP remains a funding currency.

Correlation is straightforward:

-

More cuts priced → lower UK front-end yields → GBP underperformance

-

Pushback on cuts → GBP short-covering

Bias: GBP downside capped only if the BOE leans hawkish in its guidance. Otherwise, rallies fade.

3. ECB STAGNATION — EUR STILL THE WEAK LINK

The ECB is expected to hold, but the message matters: a prolonged pause framed as patience, not confidence. Europe’s problem isn’t inflation—it’s growth. Higher yields without growth traction are EUR-negative, not supportive.

If euro area yields drift higher on reduced cut expectations while US yields stay elevated, rate differentials still favour USD. The euro does not win in a world of higher real rates unless growth surprises—and it hasn’t.

Correlation remains intact:

-

Wider US-EU yield spreads → EUR/USD lower

-

ECB pause ≠ EUR support

Bias: EUR rallies remain selling opportunities.

BOTTOM LINE

This is a rates-driven FX week. If US data holds up, the market is forced back into the Fed’s camp, yields rise, USD strengthens, and carry trades wobble. If data breaks, only then does the USD downside open—and that requires multiple misses.

Default positioning:

-

Long USD vs EUR and JPY

-

GBP tactical only, direction set by BOE guidance

-

Fade EUR strength on rallies

The market won’t fall in line voluntarily. The data will decide who blinks.

4. BOJ: HIKE DELIVERED, GUIDANCE DOES THE DAMAGE

The Bank of Japan is expected to hike rates to 0.75% at week’s end. The data backdrop gives them cover: business confidence remains firm and CPI is hovering around 3%, well above comfort levels. Markets are already there—~92% of a hike is priced via swaps, making the BOJ move more fully discounted than the expected BOE cut.

That leaves JPY trading the message, not the move.

The political risk has faded. A weak yen and rising living costs have forced the new prime minister to soften resistance to higher rates, effectively clearing the runway for a hike. USD/JPY has gone nowhere for a month because the market is waiting for policy direction, not the headline decision.

The correlation is clean:

-

Hike + cautious guidance → limited JPY upside

-

Hike + hint of follow-through → USD/JPY breaks lower

We expect the BOJ to stay deliberately vague, refusing to pre-commit to further hikes. That caps near-term JPY strength. Key downside support in USD/JPY sits at 154.20 (50-day SMA)—a break requires either hawkish guidance or a broader USD selloff.

BALANCE SHEET RISK: ETF SALES ARE A SECOND-ORDER JPY DRIVER

The BOJ may also flag the start of ETF sales from early 2026, testing an exit from its enormous equity holdings. Any sales will be glacial. The objective is explicit: zero market impact.

Japanese equities have surged over the past two years, inflating the value of these holdings and giving the BOJ room to experiment. Initial sales could begin as early as January. If markets absorb them quietly, the programme continues; if volatility spikes, it stops. This is not QT in the Western sense—it’s balance-sheet optics.

FX implications are indirect:

-

ETF sales → mild equity headwinds → limited JPY support

-

Any meaningful JPY reaction only comes if sales trigger risk-off conditions

BOTTOM LINE: POLICY DIVERGENCE IS REAL, BUT JPY NEEDS CONFIRMATION

This week reinforces policy divergence: the Fed stays restrictive while the BOJ inches toward normalisation. In theory, that’s USD/JPY negative. In practice, the move only sticks if the BOJ signals that this hike is not a one-off.

Without that signal, USD/JPY drifts, not trends. With it, the pair breaks lower.

Bias:

-

Directionally cautious JPY bullish

-

Stronger conviction only on hawkish BOJ guidance

-

USD/JPY downside opens below 154.20

The hike is priced. The path is not.

XAU/USD: MACRO CORRELATIONS & TRADE SCENARIOS

Gold is trading macro, not micro. Direction is dictated by real rates, the dollar, and policy divergence, not inflation headlines in isolation.

CORE CORRELATIONS (WHAT MATTERS)

-

US REAL YIELDS (PRIMARY DRIVER)

-

Higher real yields → XAU/USD lower

-

Lower real yields → XAU/USD higher

Gold does not care about nominal hikes; it trades the opportunity cost.

-

-

USD (SECONDARY, BUT FAST)

-

Stronger USD → gold pressured, especially via EUR and JPY weakness

-

USD strength driven by front-end repricing hits gold quickly

-

-

JPY & RISK CHANNEL

-

JPY strength + falling equities → gold bid (risk-off hedge demand)

-

BOJ tightening that hurts equities indirectly supports gold

-

-

CENTRAL BANK DIVERGENCE

-

Fed restrictive + BOJ tightening = real-rate tug-of-war

-

Gold wins only if US real rates roll over

-

SCENARIO ANALYSIS (BASED ON CURRENT DATA RISK)

SCENARIO 1: US DATA HOLDS UP (BASE CASE)

Payrolls ≥ expectations, CPI sticky

-

US front-end yields push higher

-

Real yields rise

-

USD strengthens

-

BOJ hike priced, guidance cautious → JPY muted

XAU/USD OUTCOME:

-

Gold breaks lower or remains capped

-

Rallies sold into

-

Best expression: short XAU/USD on strength

Correlation chain:

Strong US data → higher real yields → stronger USD → XAU/USD lower

SCENARIO 2: US DATA MISSES + BOJ CAUTIOUS (MIXED)

Weak payrolls, CPI cools modestly

-

Real yields fall

-

USD softens

-

BOJ refuses to guide future hikes

-

JPY underperforms vs expectations

XAU/USD OUTCOME:

-

Gold squeezes higher

-

Gains driven by real-rate relief, not inflation fear

-

Upside limited if risk stays firm

Correlation chain:

Weaker US data → lower real yields → USD softer → XAU/USD higher

SCENARIO 3: BOJ SURPRISES HAWKISH (TAIL RISK)

Hike + hints of further tightening

-

JPY strengthens aggressively

-

Japanese equities wobble

-

Global risk sentiment deteriorates

-

USD/JPY breaks lower

XAU/USD OUTCOME:

-

Gold rallies as risk hedge + FX hedge

-

Strongest upside scenario even without weak US data

Correlation chain:

Hawkish BOJ → JPY strength + risk-off → XAU/USD bid

SCENARIO 4: DUAL SHOCK RISK-OFF (LOW PROBABILITY, HIGH PAYOFF)

Weak US data + hawkish BOJ

-

Real yields fall sharply

-

USD sells off

-

Equities correct

-

Volatility spikes

XAU/USD OUTCOME:

-

Breakout move higher

-

Gold regains role as macro hedge

Correlation chain:

Falling real yields + risk-off → XAU/USD explosive upside

TRADEABLE TAKEAWAYS

-

Gold is short real yields, not long inflation

-

As long as US data holds, XAU/USD rallies are selling opportunities

-

BOJ hawkish surprise is the hidden upside catalyst

-

Watch US 10y real yields + USD/JPY for early signals

POSITIONING BIAS

-

Base case: Tactical bearish XAU/USD

-

Upside hedge: Long gold via options into US data/BOJ risk

-

Invalidation: Sustained drop in US real yields

Gold doesn’t move first. Rates do.

XAUUSD Spot Gold: $4444/4545/4646 or $4141/4040/3939 before 26 January 2026?