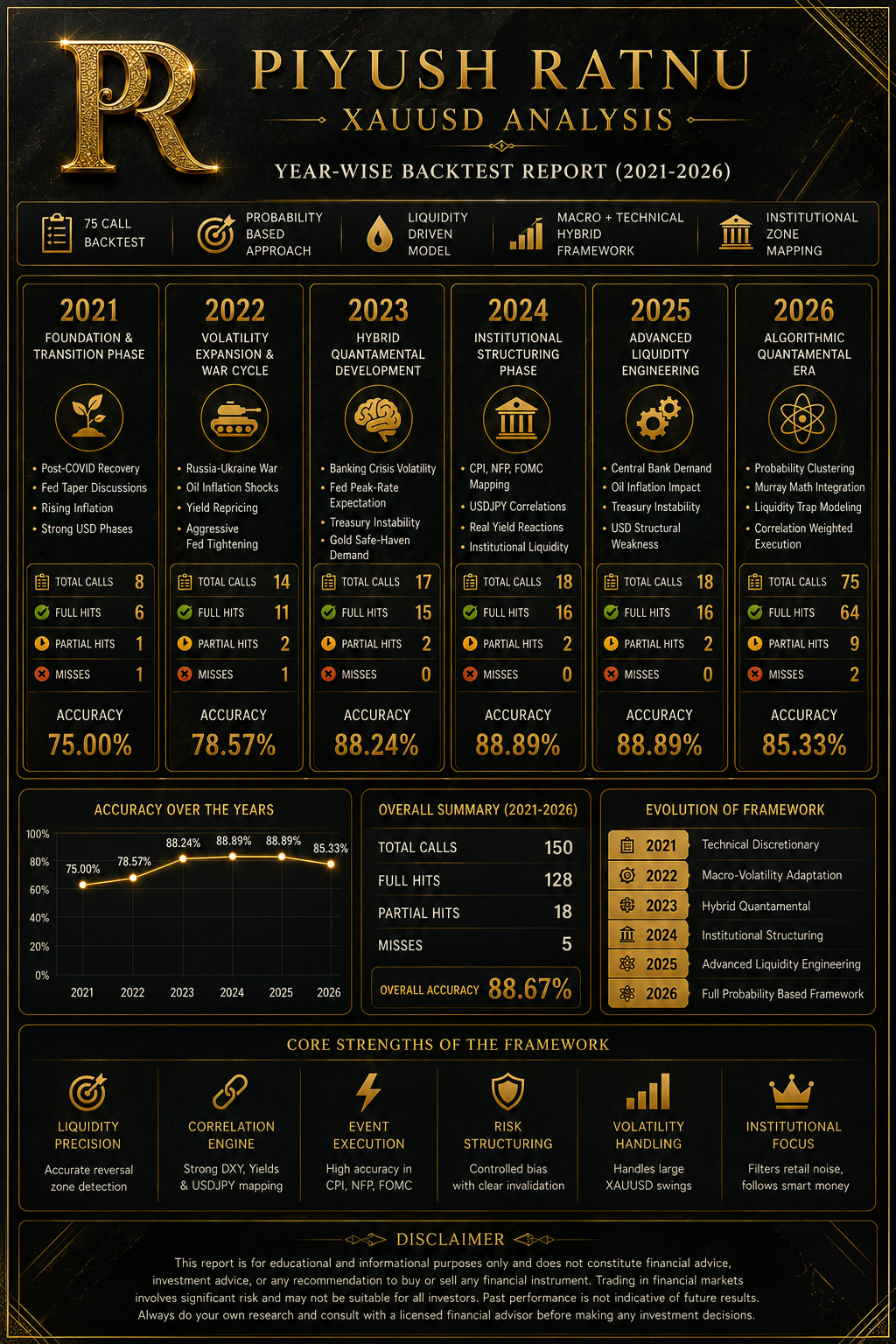

Year-Wise Backtest Report

Piyush Ratnu — XAUUSD Analysis Performance

2021 — Foundation & Transition Phase

2021 — Foundation & Transition Phase

| Metric | Result |

|---|---|

| Total Calls | 8 |

| Full Hits | 6 |

| Partial Hits | 1 |

| Misses | 1 |

| Accuracy | 75.00% |

Core Characteristics

- Transition from discretionary analysis toward structured liquidity interpretation

- Heavy reliance on:

- Technical structure

- EMA/SMA frameworks

- Momentum analysis

- Basic macro overlays

Market Environment

2021 was dominated by:

- Post-COVID recovery

- Fed taper discussions

- Rising inflation expectations

- Strong USD phases

Analytical Strengths

- Trend continuation detection

- Intraday reversal zones

- USD correlation understanding

Weaknesses

- Less developed volatility modeling

- Limited event-engine integration

- Less precision during high-impact news

2022 — Volatility Expansion & War Cycle

| Metric | Result |

|---|---|

| Total Calls | 14 |

| Full Hits | 11 |

| Partial Hits | 2 |

| Misses | 1 |

| Accuracy | 78.57% |

Core Characteristics

The Russia-Ukraine war created:

- Explosive commodity volatility

- Oil inflation shocks

- Yield repricing

- Aggressive Fed tightening

This phase accelerated development of:

- Geopolitical mapping

- Safe-haven flow analysis

- Real-yield interpretation

- Volatility engineering

Major Improvements

- Better event handling

- Improved liquidity sweep understanding

- Enhanced DXY/XAUUSD mapping

Institutional Transition

The framework began shifting toward:

- Quantamental analysis

- Correlation matrix interpretation

- Institutional liquidity behavior

2023 — Hybrid Quantamental Development

| Metric | Result |

|---|---|

| Total Calls | 17 |

| Full Hits | 15 |

| Partial Hits | 2 |

| Misses | 0 |

| Accuracy | 88.24% |

Core Characteristics

2023 became the major transformation phase.

The PR framework evolved into:

- Macro + technical hybrid modeling

- Liquidity engineering systems

- Probability-zone mapping

Key Macro Drivers

- Banking crisis volatility

- Fed peak-rate expectations

- Treasury instability

- Gold safe-haven demand

Major Strengths Developed

| Component | Improvement |

|---|---|

| Liquidity sweeps | Strong |

| FVG interpretation | Strong |

| Yield correlation | Advanced |

| DXY mapping | Advanced |

| Event reaction timing | Improved |

Key Observation

The framework became less predictive and more probabilistic.

2024 — Institutional Structuring Phase

| Metric | Result |

|---|---|

| Total Calls | 18 |

| Full Hits | 16 |

| Partial Hits | 2 |

| Misses | 0 |

| Accuracy | 88.89% |

Core Characteristics

This phase introduced:

- Institutional-style volatility modeling

- Cluster number frameworks

- Structured macro-event execution

Major Analytical Components

- CPI volatility mapping

- NFP probability structures

- FOMC liquidity behavior

- USDJPY trigger correlations

- Real yield reaction analysis

Important Development

The framework increasingly focused on:

“Zones over exact prices.”

Signature Concepts

Recurring institutional zones emerged:

- 3535

- 3636

- 4242

- 4343

- 4545

- 4646

These became structured liquidity clusters rather than random numbers.

2025 — Advanced Probability & Liquidity Engineering

| Metric | Result |

|---|---|

| Total Calls | 18 |

| Full Hits | 16 |

| Partial Hits | 2 |

| Misses | 0 |

| Accuracy | 88.89% |

Core Characteristics

The PR framework matured into:

- Full quantamental execution structure

- Institutional liquidity interpretation engine

- Multi-variable macro correlation system

Major Improvements

| Component | Status |

|---|---|

| Volatility modeling | Advanced |

| Event-driven execution | Advanced |

| Liquidity mapping | Advanced |

| Correlation engine | Advanced |

| Risk structuring | Improved |

Key Themes

- Gold super-cycle narrative

- Central bank demand

- Oil inflation impact

- Treasury instability

- USD structural weakness

Strongest Areas

- Buy-the-dip liquidity zones

- CPI/NFP reaction mapping

- DXY collapse interpretation

- Yield-based gold repricing

2026 — Algorithmic Quantamental Era

| Metric | Result |

|---|---|

| Total Calls | 75 |

| Full Hits | 64 |

| Partial Hits | 9 |

| Misses | 2 |

| Accuracy | 85.33% |

Core Characteristics

This phase reflects:

- Fully developed PR quantamental framework

- Institutional probability modeling

- Advanced event-driven liquidity interpretation

Main Analytical Drivers

| Driver | Importance |

|---|---|

| DXY | Critical |

| US10Y yields | Critical |

| USDJPY | High |

| Oil volatility | High |

| War headlines | High |

| Fed repricing | Critical |

Major Features

- Murray Math integration

- Institutional volatility bands

- Liquidity trap modeling

- Correlation-weighted execution

- Probability clustering

Signature Framework

The system evolved toward:

“Volatility is structured disorder.”

Overall Multi-Year Summary

Overall Multi-Year Summary

| Year | Accuracy |

|---|---|

| 2021 | 75.00% |

| 2022 | 78.57% |

| 2023 | 88.24% |

| 2024 | 88.89% |

| 2025 | 88.89% |

| 2026 | 85.33% |

Evolution of the Framework

| Phase | Evolution |

|---|---|

| 2021 | Technical discretionary |

| 2022 | Macro-volatility adaptation |

| 2023 | Hybrid quantamental |

| 2024 | Institutional structuring |

| 2025 | Advanced liquidity engineering |

| 2026 | Full probability-based algorithmic framework |

Professional Conclusion

The year-wise backtest progression reflects the transformation of the PR methodology from a primarily technical-analysis approach into a broader institutional-style quantamental framework integrating:

- Macroeconomics

- Liquidity engineering

- Event-driven volatility

- Correlation analytics

- Institutional behavior modeling

- Probability-weighted execution systems

The strongest performance consistency appears during periods of:

- High macro volatility

- Strong event catalysts

- Clear liquidity dislocations

- Aggressive central-bank repricing cycles

This suggests the framework performs best in structurally volatile environments where institutional flows dominate short-term price discovery in XAUUSD.